What Do Past Shocks Tell Us About the Choices We’ll Face After the Pandemic? A Series on Education Finance Post-COVID

What Do Past Shocks Tell Us About the Choices We’ll Face After the Pandemic? A Series on Education Finance Post-COVID

While much of the education sector’s attention is focused on the effects of COVID-19 school closures on children’s learning and welfare, the most significant and lasting impact on education will almost certainly be as a result of the pandemic’s economic shock. This has led to urgent calls from the international community to protect—and increase—education spending in the wake of the crisis. Yet we know that despite these efforts, policymakers are going to have to make difficult tradeoffs.

RELATED EXPERTS

It’s time to shift that conversation from wishing we had more money to engaging in the tough national debates about prioritization policymakers are facing. We’ve heard the consistent refrain that the education sector needs to become more resilient to this and future crises, but we’ve heard much less about what that means in practice. Inevitably, it will require identifying tradeoffs and strategizing about how to deal with them in ways that support education outcomes, especially for students and families most likely to be affected.

In a new CGD series, we’ll be examining the evidence on how COVID will affect education finance. We want to generate policy-relevant lessons for donors and policymakers as they plan post-COVID education budgets. We’ll be taking a look at the impact of the crisis on teacher labor markets and public sector wage budgets, prioritisation of education spending by governments facing shocks in other sectors, household budgets and spending in the wake of financial and other crises, and further investigations of the impacts of crises on aid to education. Then we’ll bring it all together to create a holistic and nuanced picture of how shocks affect education budgets as well as to inform the inevitable tradeoffs governments will face—now and in future crises.

The precise impacts of the crisis will not be known for many months, but lessons from past crises and initial estimates suggest finance gaps will be substantial in low- and middle-income countries over the next several years as governments face tighter budgets and more acute public spending tradeoffs. Precisely where those cuts occur and how severely they’ll impact education outcomes, however, is likely to vary considerably across contexts.

Effects on education finance may be driven by reduced GDP and public sector budgets, potential disproportionate reduction of education budgets, reduced household spending, and cuts to education aid. The IMF projects that global growth will slow from the original estimates of 3.3 percent to -3.0 percent, resulting in a global recession. A reversal in growth could result in substantially larger gaps in funding for education needed to reach the SDGs from both domestic and international sources than previously estimated.

At the start of the current crisis, CGD colleagues estimated that if the government proportion of education spending remains the same (between 3.7 percent and 4.7 percent of GDP in low- and middle-income countries), combined with the current growth projections, total education spending in middle income countries could drop by 2-4 percent post-COVID. That would risk lasting negative impacts on education outcomes, particularly in the poorest countries. Countries reliant on export commodities, including Angola and Nigeria, may be hit especially hard.

At the same time, the costs associated with schooling may rise—at least in the short-run—as countries work to implement large-scale distance learning, remediation, and re-enrollment programmes as well as new health and safety measures to protect students as schools reopen. For example, the WHO and UNICEF recommend physical distancing and the provision of PPE in schools in order to ensure safe reopening. However, prior to the pandemic more than 40 percent of schools globally lacked handwashing facilities, and only a quarter of schools in sub-Saharan Africa had basic hygiene facilities. In sub-Saharan Africa, at least nine countries have average pupil-teacher ratios greater than 50 at the primary level, which will likely make physical distancing challenging when schools reopen, unless there are additional classrooms and teachers.

On top of needing more teachers and space to maintain physical distance for students previously enrolled, we may also see an increase in the number of students in public school systems as families facing economic shocks move children from private to public schools.

2. Public sector wage bills, including public school teacher salaries, are likely to be protected in many places. But this may come at a cost.

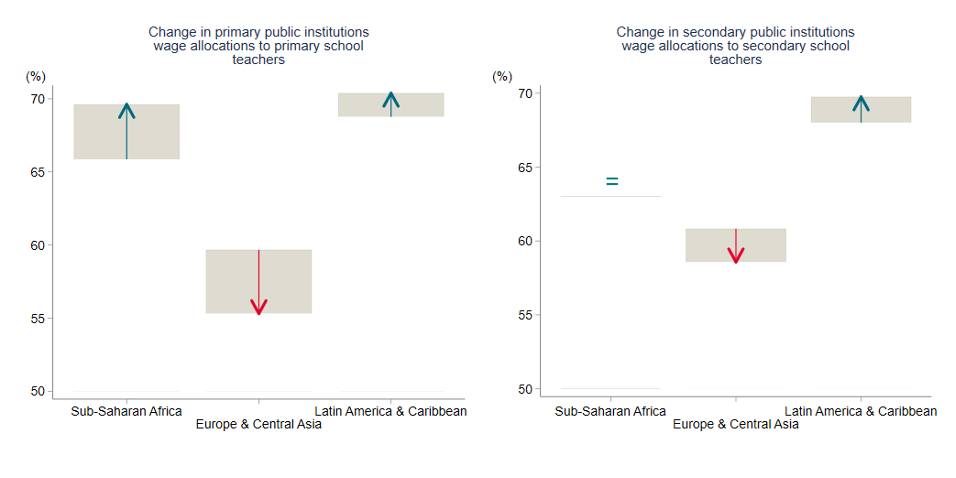

Evidence from past recessions and other crises suggests that public sector wage bills—which include teacher salaries—are procyclical (i.e., they are likely to contract following the crisis). However, we may not see consistent impacts across contexts. The figure below shows that while teacher salaries in Europe and Central Asia contracted following the global financial crisis, salaries increased or remained constant in sub-Saharan Africa and Latin America.

Figure 1. Changes in primary and secondary teacher salary allocations following the global financial crisis (as a percentage of total expenditure in primary and secondary public institutions)

Source: authors’ analysis of UIS data

Note: averages consider two years before and after the crisis. Also includes 13 Sub-Saharan African countries, 17 European and Central Asian countries, and 10 Latin American and Caribbean countries

Though salaries for civil service teachers may be protected, emerging evidence from the current crisis suggests that salaries of private school and fixed-term contract teachers—which make up a large portion of the education workforce in some places—are at risk. The wage gap between permanent civil servants and fixed-term teachers was already substantial across sub-Saharan Africa, and contract teachers may be more likely to work in more disadvantaged and remote locations—meaning that their departure could stretch teacher shortages in poorer and rural areas.

Focusing too narrowly on protecting civil service teacher salaries in the wake of the pandemic may come at the expense of the wider education workforce or other critical areas of the education budget.

3. We don’t know yet whether COVID-19—a global health crisis—will disproportionately impact resources in the education sector

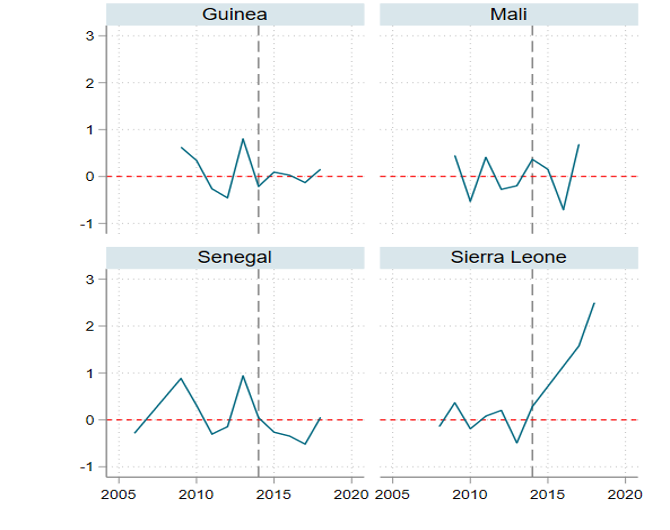

We know that financial shocks can negatively impact social spending. But what happens to education budgets when there is an urgent health shock that results in a financial crisis? Intuitively, we might expect to see a substitution effect in which governments with limited resources are forced to choose health over education (at least in the short-term) to address the most urgent needs. And in fact we’ve already seen some evidence of this, as several countries including Azerbaijan, Bulgaria, Ecuador, Kenya, Nigeria, and Ukraine have proposed cuts to education spending to support health or other stimulus activities. In Nigeria, cuts of up to 45 percent have been proposed to the federal Universal Basic Education Commission. Evidence from past health crises indicates that this will not necessarily be the case everywhere, and while we’ve seen cuts in some places thus far, we’ve also seen many countries introduce additional financing to support education during the pandemic. While the data available are noisy, the figure below shows varying impacts on education spending following the Ebola crisis. We plan to explore this relationship in more detail—and across more crises—in the coming weeks.

Figure 2. Change in government expenditure on education (percent GDP change) after the Ebola crisis

Source: authors’ analysis of UIS and WHO data

4. Impacts on education spending at the household level will vary across and within countries

In the face of already stretched household budgets, shocks are likely to increase the financial burdens families face in sending children to school, particularly in places in which households must make up for reductions in government spending. We’ve already seen many instances of reduced household income and consumption over the past seven months, as well as substantial negative impacts on work and livelihoods. Evidence from past crises suggests that household responses, however, are likely to vary based on whether the shock has an income or substitution effect—e.g., it creates a surplus or shortage of time or money—at the household level as well as on household perceptions of the role of education in overcoming the shock.

For example, following the East Asian financial crisis (an aggregate shock) in the 1990s, many households increased expenditure on education as government resources became more constrained, while household-level economic shocks have been linked to reductions in education spending and participation. In the case of the East Asian crisis, the additional financial burden placed on households to make up for government shortfalls worsened pre-existing inequalities.

5. Countries and households with higher rates of remittances may be hit harder

In 2019, remittances were estimated to be the largest source of external financing to low- and middle-income countries. Not only can remittances be an important source of household income for families in low- and middle-income countries, they can impact participation in primary and secondary education. Remittances sent to developing countries are projected to decrease by 23 percent this year, which may have negative income effects for recipient households, limiting ability to make up for shortfalls in government spending on health and education. In 2019, the top remittance recipients included China, Egypt, India, Philippines, and Mexico.

Following the global financial crisis in 2009, remittances sent to Mexico decreased by 20 percent and dropout rates nearly doubled for 12-16-year-olds in households that received remittances.

6. International aid is likely to contract, so donors should prioritize the poorest countries as well as those in which alternate sources of education finance are likely to be most affected

A recession will constrain aid budgets in high-income countries, and the pandemic heightens pressure to prioritize needs at home. Public support for international aid typically decreases in donor countries during recessions, though there is some evidence that aid for social and humanitarian sectors are more likely to be protected than aid for other sectors. The extent to which donors will move funds previously allocated to education to support the health sector following the current crisis remains unclear.

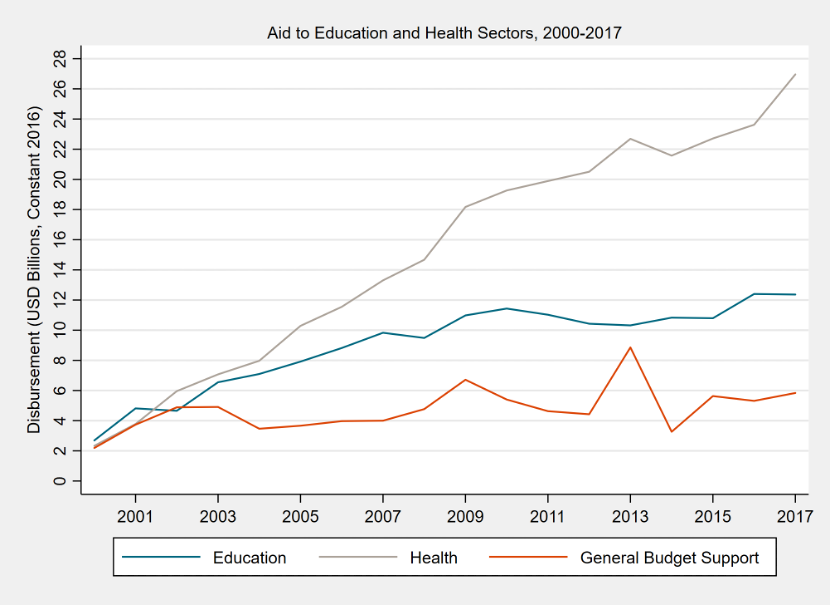

Following the global financial crisis, total international aid remained relatively constant, but the share allocated to education decreased while the share to health increased. An analysis by UNESCO predicts that aid to education could drop by as much as 12 percent over the next two years. Francisco Ferreira and Norbert Schady argue that human capital investments suffer most in the poorest countries following shocks and that the best way to protect and support education outcomes is to prioritize allocations that are biased toward the poorest countries, and those that have the least developed credit markets.

Figure 3. Total sector allocable aid and shares allocated to health and education over time

Source: CGD analysis using data from OECD DAC Creditor Reporting System.

7. Across the financing architecture, impacts of the shock are likely to be driven by equal parts economic and political considerations

Difficult decisions on tradeoffs are inherently political at all levels. Donor countries will have to balance competing demands at home with increasingly urgent calls for support in developing countries. Governments will have to balance cross-sectoral demands for resources and answer to voters. The poor (who may benefit most from publicly provided services) are often the least likely to be considered a critical voting constituency, and the most marginalized (e.g., refugees, students with disabilities) may be disproportionately affected by government finance decisions. Within the education sector, teachers’ unions and other interest groups may try to shape the extent and nature of budget cuts and will likely try to protect teacher salaries—and particularly those of civil servant and union members—over and above other areas of education spending.

Watch this space for more on education finance and shocks coming soon.

Thanks to Ana Minardi for helpful contributions.

RELATED TOPICS:

DISCLAIMER

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

0 Comments